No one else can tell you that you’re ready to be a homeowner. This is one of the largest purchases many consumers will ever make. It’s something most of us do just a handful of times in our lives.

For many people, the right time is when they feel financially and emotionally ready for the responsibility. That’s not always easy to discern, especially for first-time homebuyers.

It’s essential that prospective homebuyers take steps to prepare for the financial responsibilities of homeownership.

5 Financial Tips for Buying a Home

Let’s take a look at a few key things you can do to prepare yourself better.

1. Build a Budget

A budget helps you set and save for financial goals and determine if you can manage a mortgage payment. It's key to know how much money you earn and spend every month when preparing to buy a home. Without a budget, It’s tough to know what kind of mortgage payment you can afford.

Consider your long-term plans. Ensure that the home you're buying aligns with your future goals: family expansion, career changes or lifestyle adjustments. One common rule of thumb is to expect it to take around 5 to 7 years to break even on a home purchase.

There are countless strategies, tools and best practices when it comes to budgeting. The goal is to figure out what works best for you while still giving you a clear, realistic picture of your finances.

Some people use simple spreadsheets to track their monthly spending, while others use online tools and apps. Two popular choices are Mint.com and You Need a Budget. With these tools, you can easily enter expenses as you make them. Some even let you connect all your financial accounts in one place. This form of real-time budgeting has become increasingly powerful for many would-be homebuyers.

2. Keep Track of Expenses

Whatever your budgeting method, what’s vital is knowing where your money goes each month. Log all of your expenses over the last month or more, making sure you don't miss small things like ATM fees. It may be easier to start by grouping them into categories.

Some common categories include:

- Housing

- Loans (like student or car loans)

- Credit cards

- Food

- Transportation (gas money, car insurance, metro card, etc.)

- Clothing

- Entertainment

- Utilities

- Occasional costs (holidays, vacations, etc.)

- Unexpected costs (car repairs, medical bills, etc.)

Your budget should accurately reflect your specific financial situation and savings goals. It’s one of the most efficient ways to see where to cut costs and increase savings.

Once you see all of your monthly expenses, you can set new spending goals. Let’s say you want to cut your overall spending by 10%, build an emergency fund and start saving for a home purchase. Run through your expense categories and look for simple ways to cut costs and start saving.

Some ways you might be able to limit spending include:

- Buy groceries in bulk and plan meals instead of eating out

- Try to negotiate better deals or downgrade plans for services like TV or Internet

- Carpool or use public transportation

- Review and possibly cancel some memberships or subscriptions

- Purchase from thrift stores rather than buying new

Some people assign every dollar they earn to specific needs, such as bills, groceries or saving for a house. Automatic withdrawals and bill pay can help make it easier to dedicate those dollars every month.

Others use an envelope system, paying for certain things in cash. For instance, once the "food" envelope is empty, no more spending on that until the next paycheck.

Choose a method that suits you, but be realistic and flexible. Set aside a bit for "fun" every month. Having some flexibility helps you stick to your budget without feeling trapped. Remember, smart budgeting is about giving you more financial freedom.

3. Get Debt Under Control

You don’t need to be debt-free to land a home loan. But lenders will calculate a debt-to-income (DTI) ratio based on your gross monthly income and major debts, including your new projected mortgage payment. For example, if your gross monthly income is $4,000 and your major monthly debts are $1,800, that’s a 45% DTI ratio (1,800/4,000).

Ideally, the VA prefers a DTI ratio under 41%. A higher ratio might require particular financial conditions. Different lenders can have different caps for DTI ratio, but the higher your ratio, the tougher it can be to secure financing.

In addition, some types of debt can be more troublesome than others. Lenders may have an in-house cap on how much “derogatory credit” borrowers can have. Derogatory credit refers to negative information on a person's credit report, which often indicates serious delinquency or late payments. These can include things like collections, charge-offs, judgments and liens.

Whether it’s $5,000 or $15,000 or more, these derogatory credit caps can vary by lender. Some of these issues must be satisfactorily addressed before a loan can close. That often means either paying the sum in full or establishing a repayment plan and a history of on-time payments.

The bottom line is: Your major monthly debts will play a big role when lenders look at what you can afford and how much home you can buy.

As with budgeting, there are multiple approaches and strategies out there for how best to pay down debt.

Some common ways to reduce debt include:

- Pay off the highest-interest debt first, typically credit cards.

- Move high-interest balances to a pre-existing credit line with a lower rate. Be mindful of transfer fees.

- Always pay more than the minimum. Minimum payments mainly prolong your debt.

- Start by paying off the accounts with the smallest balances and work your way up to the largest. Use the “little victories” method to build momentum.

- Avoid new debts. Follow your budget and save for emergencies so you don’t need to use credit cards unexpectedly.

- Sell unused items and use the money for debt repayment.

- Stay away from short-term loans like payday loans due to high interest. Also, be cautious when co-signing loans for others.

Establishing a realistic budget is a key early step before you decide how best to tackle your debts. Set monthly savings goals that include funds earmarked for debt repayment. Finding the right strategy is important, but you also need the available cash to make those payments every month. You can’t do that effectively without a good budget in place.

4. Practice Your Mortgage Payment

Trying out a mortgage "test run" can show you if you're ready for a home loan. Our VA Loan Calculator can help you figure out your estimated monthly payment.

Let’s say you’re paying $800 a month in rent, and the kind of home you’d like to buy will have a mortgage payment of roughly $1,200. That’s a $400 difference. Over the course of the next few months, pay your rent and then take an additional $400 and put it in a savings account.

Live as if that $400 is already going towards a mortgage. If you're comfortable without it, you might be ready for that house payment. If not, you might need to adjust your budget or consider a cheaper home.

What if you don’t have housing expenses right now? If you’re living with a family member or friend rent-free, lenders may be concerned about “payment shock” with a new mortgage. Ideally, prospective buyers who haven’t been burdened with a rent payment should have been able to build up savings.

Those who haven’t socked away money thanks to their rent-free arrangement may come under closer scrutiny. Lenders may wonder: If you haven’t been paying rent for 12 months, why don’t you have 12 months of rent saved up? How will you be able to afford your new $1,000 monthly mortgage payment when you weren’t saving $1,000 a month in rent?

This is where assets and reserve funds can play a key role in showing mortgage lenders you’re ready for the financial responsibility of a home loan.

5. Build Reserves

Owning a home comes with upfront costs. In most cases, there’s no set amount of assets you’ll need in the bank to begin this journey, but lenders will want to make sure getting a loan doesn’t put a strain on your finances.

If you are looking to buy a home, you need to truly understand the costs that come with owning a home and make sure you can afford it. Too many people buy too much house and then get cash-strapped once repairs and upkeep come into play.

It's wise to save at least three months of living expenses in a separate account before buying a home. This "emergency housing fund" or "reserves" should be easily accessible for unexpected events like job loss or medical emergencies. Having these reserves not only provides a safety net but also impresses lenders.

There can also be situations when lenders will require you to have a certain number of months' worth of reserves in the bank. A couple of common examples are if you’re seeking a jumbo loan or buyers who aim to count rental income toward qualifying for a new mortgage.

As prepared as you might be, a lender still has to decide if you’re ready to handle a mortgage. A big part of the evaluation hinges on your credit profile. With careful financial planning, you can make mortgage payments a seamless part of your monthly expenses. You'll be financially equipped to handle it confidently.

» CALCULATE: Calculate your VA Loan savings

How much money should be saved before buying a house?

When planning to save for a home, aim to set aside approximately 5% of the purchase price. This should help cover relocation expenses and any closing costs the sellers aren’t willing to pay. Ideally, you would also have 3 to 6 months of regular living expenses saved for an emergency fund in addition to this amount.

Get Preapproved!

Once you have your budget under control, mortgage preapproval is a crucial step. Not only does it provide a clear understanding of what you can afford, but it also positions you as a serious buyer in the eyes of sellers, giving you a competitive edge in today's fast-paced market.

Preapproval can be the difference between securing your dream home and watching it slip through your fingers. So, before diving deep into your house hunt, take a moment to get preapproved — it might just be your key to a seamless home-buying experience.

Related Posts

-

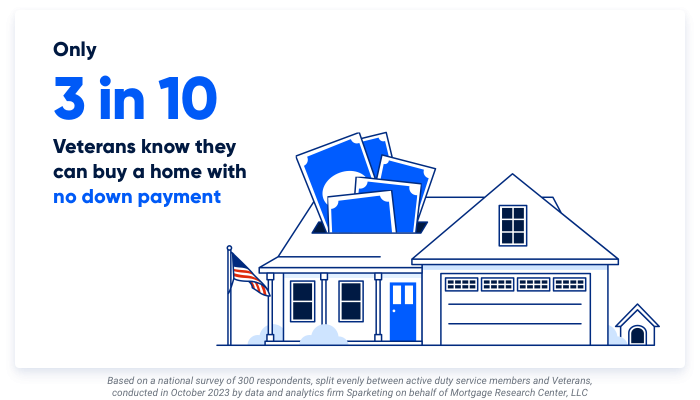

VA Loan Down Payment RequirementsVA loans have no downpayment requirements as long as the Veteran has full entitlement, but only 3-in-10 Veterans know they can buy a home loan with zero down payment. Here’s what Veterans need to know about VA loan down payment requirements.

VA Loan Down Payment RequirementsVA loans have no downpayment requirements as long as the Veteran has full entitlement, but only 3-in-10 Veterans know they can buy a home loan with zero down payment. Here’s what Veterans need to know about VA loan down payment requirements. -

VA Loan vs Conventional Loan: A Complete ComparisonHere we compare the primary differences between VA and conventional loans to show you when each option may be the best.

VA Loan vs Conventional Loan: A Complete ComparisonHere we compare the primary differences between VA and conventional loans to show you when each option may be the best.